Wondering how to create and edit DOCX documents without MS Word? Try Writer's all-new desktop app!Posted on August 22, 2023August 22, 2023 by Raksha4 Mins Read

Mastering harmonious exchange: Five internal communication behaviors for seamless workplace dynamicsPosted on August 22, 2023August 22, 2023 by Shanthana Lakshmi S4 Mins Read

Mastering the data maze: Exploring business intelligence within Zoho One, Part 2Posted on August 16, 2023August 16, 2023 by Mani Prabhu6 Mins Read

Video messages: The game-changer in your team communicationPosted on August 16, 2023August 16, 2023 by Jane Cynthia4 Mins Read

AI's transformative impact on business intelligence and its role in predictive analyticsPosted on August 11, 2023August 11, 2023 by Pradeep V6 Mins Read

App Spotlight: Driving Licence Validation for Zoho CRMPosted on August 11, 2023August 11, 2023 by Reena Makwana2 Mins Read

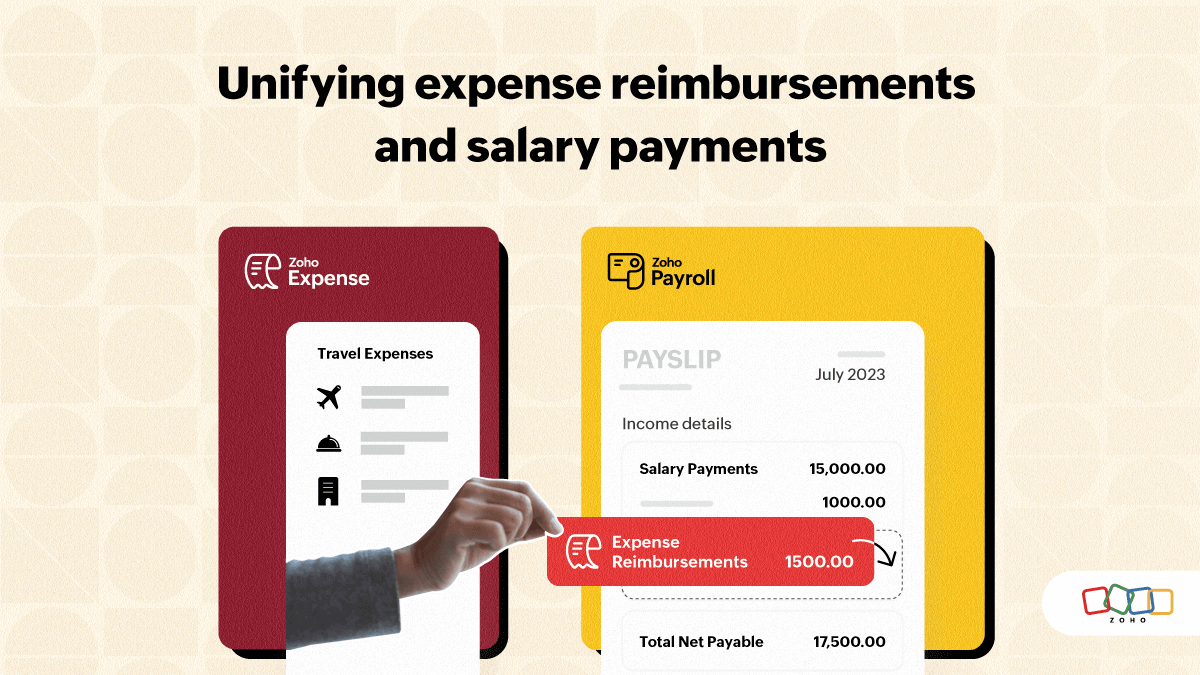

Simplifying your employee payments: Combine expense reimbursements and salary payments with ZohoPosted on August 10, 2023August 10, 2023 by Bennet Noel4 Mins Read

Connect your Zoho Calendar with 5,000+ applications through ZapierPosted on August 10, 2023August 10, 2023 by Prashanth4 Mins Read

Zoho Tasks is now Zoho ToDo: Introducing exciting features and an all-new mobile appPosted on August 9, 2023August 9, 2023 by Pearlyn Anugraha6 Mins Read

How does PAN Details Retrieval for Zoho CRM benefit businesses? Posted on August 9, 2023August 9, 2023 by Reena Makwana3 Mins Read

Types of work schedules you need to know as a business ownerPosted on August 9, 2023August 9, 2023 by Pramod7 Mins Read

App Spotlight: Jotform Sign for Zoho CRMPosted on August 8, 2023August 8, 2023 by judith.f3 Mins Read

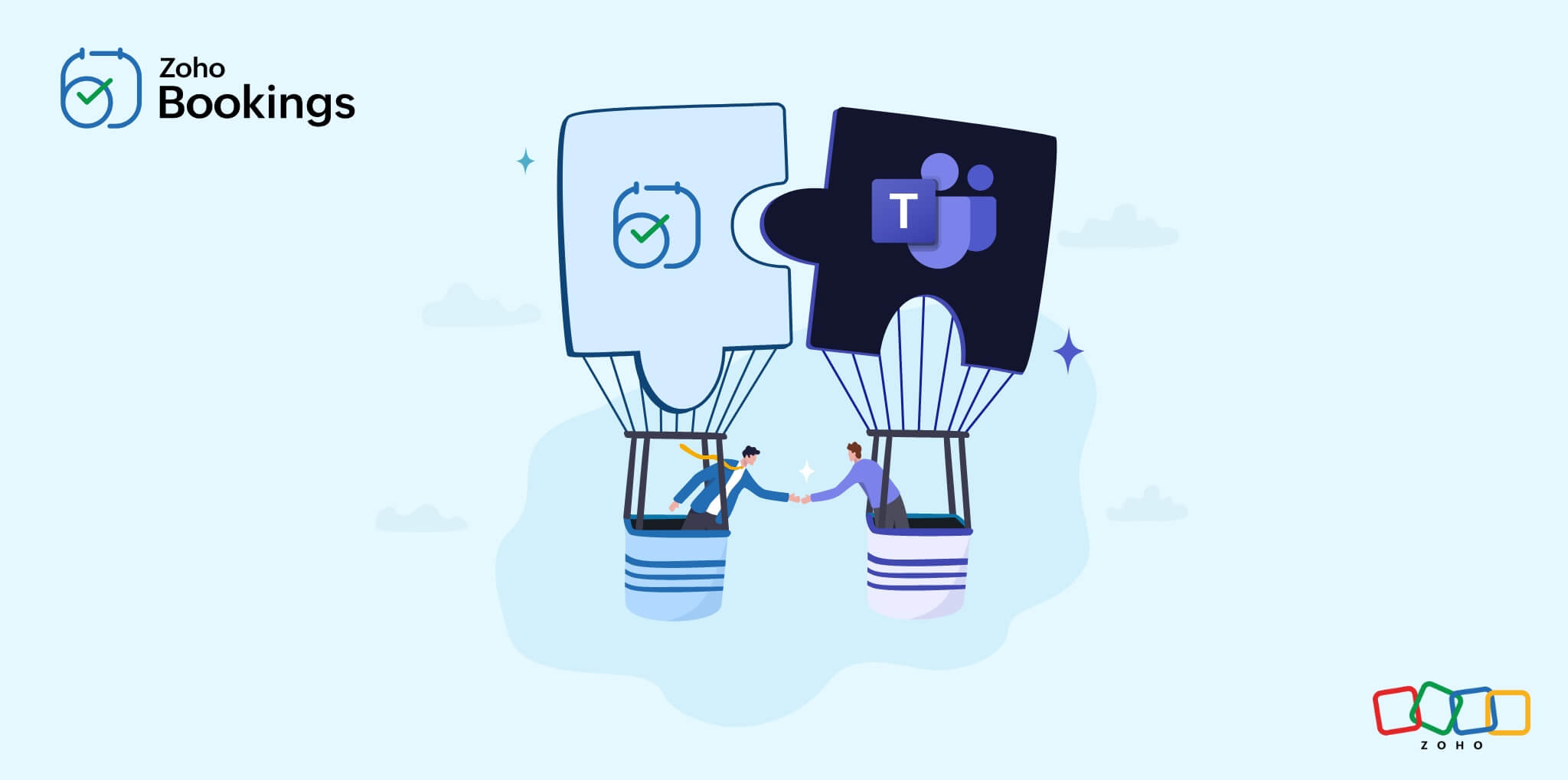

Schedule seamless online meetings with the Microsoft Teams and Zoho Bookings integration Posted on August 8, 2023August 8, 2023 by Ela3 Mins Read

Enhance business productivity with automatic prefilled form generationPosted on August 8, 2023August 8, 2023 by Sathish6 Mins Read

App Spotlight: PAN Details Retrieval for Zoho CRMPosted on August 8, 2023August 8, 2023 by Reena Makwana2 Mins Read

Organize and conquer: Seamless conversations with Zoho CliqPosted on August 8, 2023August 8, 2023 by Farheen Fathima3 Mins Read

Customer-centric support: How Zoho Assist and LiveChat can transform your businessPosted on August 7, 2023August 7, 2023 by Steffi4 Mins Read

Celebrating an eventful 5 years of Zoho Backstage!Posted on August 4, 2023August 4, 2023 by Lavanya4 Mins Read

Zoho Vault recognized as a Challenger and Fast Mover in the 2023 GigaOm Radar for Password Management Posted on August 4, 2023August 4, 2023 by Rishit Chithirala6 Mins Read

Introducing exciting new features to enhance your calendar experiencePosted on August 3, 2023August 3, 2023 by Janani Seshadri4 Mins Read